Workplace Hunch Will get Ugly in Houston, San Francisco, Los Angeles, Manhattan, Chicago, Washington DC

This is not a slip up.

By Wolf Richter for WOLF STREET.

Houston has been the toughest major office market for landlords for years after a historic boom in office tower construction clashed with the Great American Oil Bust, which began in 2015, and hit a maddened spell in April 2020 that briefly collapsed the reference WTI for crude oil quality minus $ 37 per barrel on the futures market. Hundreds of oil and gas companies filed for bankruptcy in 2020, most of them in Texas. Added to this was the relocation of the pandemic from home.

With the announcement of their plans, it is becoming increasingly clear that there will be a long-term hybrid model in which some employees work from home permanently, others work in the office almost all of the time, and many others work from home all the time and temporarily immersed themselves in the Office open, with hot desking and large lounge meeting areas taking over desk farms. And companies can reduce their office requirements.

And now Houston is getting a lot of hot competition in terms of vacant office space from large, expensive office markets like San Francisco, Los Angeles, Manhattan, Chicago, Washington DC, and others.

Houston, still the toughest office market.

Available office space rose to 54.8 million square feet (msf), or 31.6% of the total, in the first quarter, according to JLL, a real estate and investment management service provider. Available space includes vacant, sublet and occupied office space that is currently being marketed as available for rent. JLL named the causes: “Bankruptcies, downsizing and layoffs.”

The total vacancy rate rose for the fifth quarter in a row and reached 26.2%. Of the 19 sub-markets, 15 recorded rental losses in the quarter (chart via JLL):

“Large blocks of sublet space continue to come out,” said JLL. In the first quarter, the availability of subleases increased to 6.4 msf.

If companies rent office space that they no longer need or no longer need due to downsizing and that have only been rented for possible future use, they can sublet the space on the market. And because they are only trying to cover part of their costs and not have to make money from the subleases, they can do so at much lower rents than direct leases from landlords. And that happens on a massive scale.

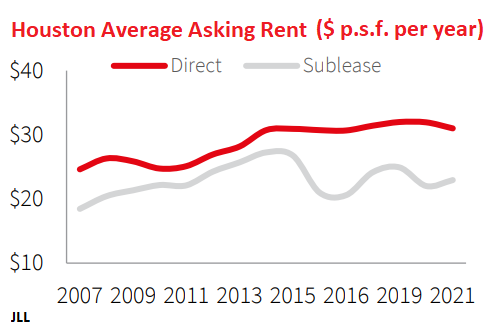

Overall, asking rents (red line) are down to $ 31 per square foot (psf) per year, but asking rents for subleases are 26% lower, at $ 22.93 psf. Advertised rents are the specified rents. However, landlords can work with their tenants to come up with a more attractive proposition, including concessions, free rent and improvement grants (graphic via JLL):

The total market-wide leasing volume in the first quarter fell from the five-year average by 66% to 1.3 msf, as “the tenants have continued to postpone the leasing decisions”.

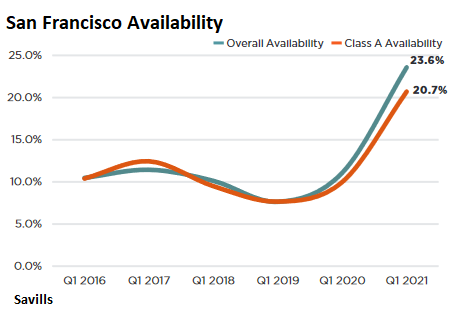

Once one of the hottest office markets, San Francisco is suddenly approaching Houston.

According to real estate service provider Savills, the number of subleases rose by a further SF 200,000 in the first quarter to a new all-time high of SF 8.9 million. Last year, San Francisco’s sublet space lost 6.4 msf in Houston, even though the Houston office market is more than double that of San Francisco.

The overall availability rate rose from the single-digit numbers two years ago to 23.6% (graphic via Savills):

“Current conditions offer users an unprecedented opportunity to secure space in what was once an incredibly tight leasing environment as owners soon have to compete with the tsunami of sublet space,” Savills said in his San Francisco Market Report. A suspected office shortage suddenly turns into a majestic office glut.

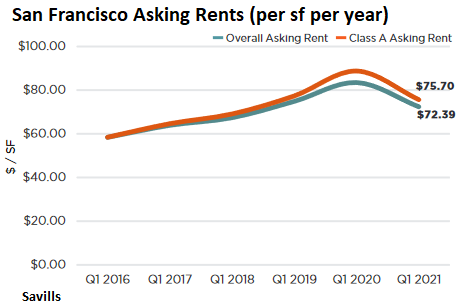

Overall, asking rents fell by 13% year-on-year and asking rents for class A fell by 15%. Savills: “In view of the flood of available space on the market, an additional decline is to be expected in the coming quarters, as the landlords move from a phase of the“ closed market ”to a phase of revaluation as soon as the tenants’ appetite for space is complete again begins to grow The sublease market is becoming a real competition. “(Diagram via Savills).

Leasing activities are rented at just 0.4 msf, a decrease of 75% compared to 1.6 msf in the first quarter of 2020 and a decrease of 85% compared to 2.5 msf in the first quarter of 2019. More than half of the leases signed were accounted for on the extension of rental agreements.

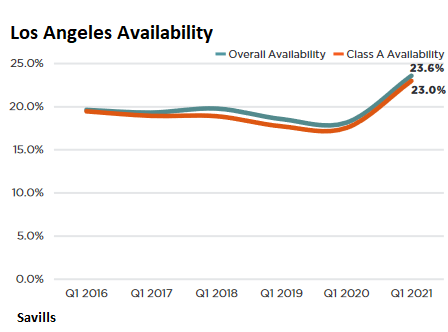

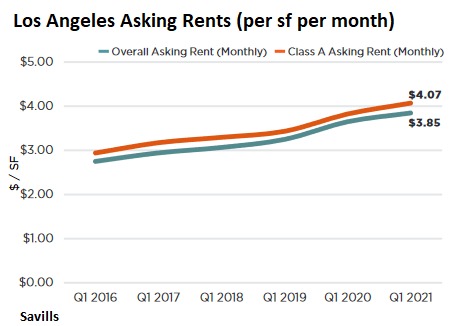

The angel.

According to Savills’ Los Angeles Market Report, office availability increased to 23.6% in the first quarter, its highest level since 2009. Sub-lease space increased to 9.0 msf. And the availability of “shade” – space that is available but not currently advertised – will be a bigger problem in 2021, especially in trophy buildings, “the report said (graphic via Savills).

The leasing activity in the first quarter fell year-on-year by 49% to 2.0 msf. However, rental demand “remains stubbornly high” rose to $ 3.85 per square foot per month (or $ 46.20 per year).

“As has been seen in the last few quarters, the currently higher asking rents are misleading, as landlords have to take aggressive action against tenants in view of the weaker market conditions. Concessions such as parking reduction and contraction rights [a right in the lease to reduce the size of the office at a future date] are widespread again and are unlikely to go away anytime soon, ”said Savills.

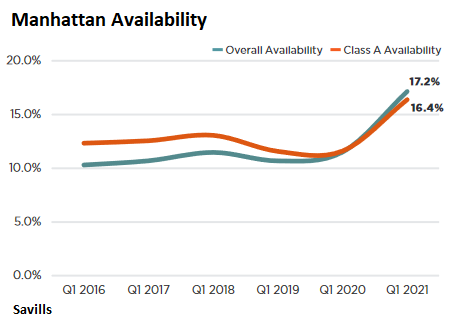

Manhattan, the biggie.

In the largest office market in the US, availability rose to 17.2%, “the highest level in at least three decades,” said Savills, “with both direct and sublet space continuing to flood the market.” The availability of subleases increased by 3.4 msf to 22 msf in the first quarter. And an additional 7.9 msf of direct storage came on the market, including “some notable additions to some shuttered coworking spaces.” (Diagram via Savills).

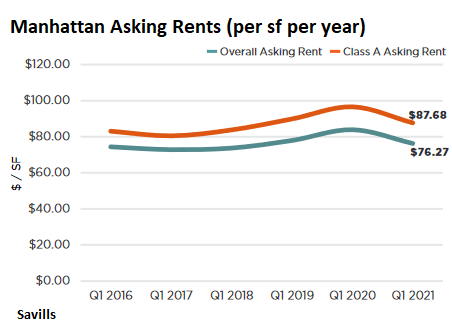

Leasing activity in the first quarter fell by 48% year-on-year and by 13.7% compared to the fourth quarter to 4.0 msf.

The average asking rent fell by 9.1% year-on-year to 76.27 psf per year. The asking rents do not include concessions that have “increased significantly” in the case of new long-term class A leases. Additionally, the average tenant improvement allowance increased 15.5% to 124.85 psf and the average free rent increased 17.4% to 13.5 months, according to Savills.

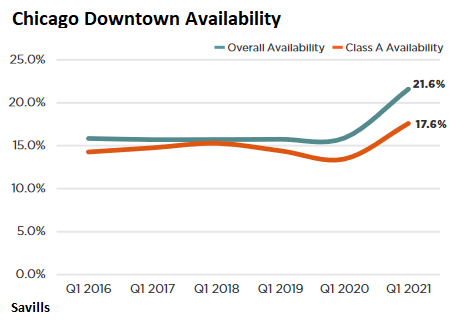

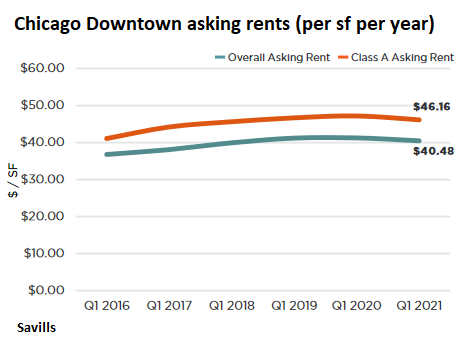

Downtown Chicago.

Overall availability rose to 21.6% and showed “no signs of slowing” according to Savills’ Chicago report. In the central loop, the availability increased to 24.3% (graphic via Savills):

Although leasing activity was stuck in collapse mode in the first quarter, declining 73.5% year-over-year, landlords haven’t moved much in terms of rental demand. “However, many landlords have shown a propensity for sharply reduced rents, increased concessions and considerable flexibility for users who are active and willing to make leasing decisions,” the report said (graphic via Savills).

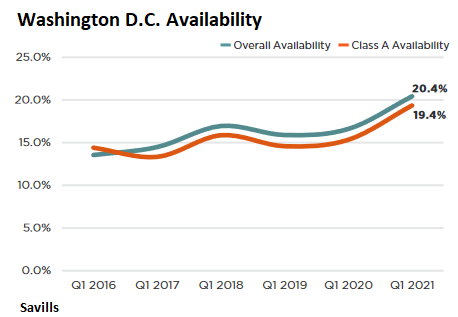

Washington DC, the government is still leasing.

Amid growing sublet space, total availability rose to 20.4%, “the highest level in at least three decades,” as “tenants are waiting to rent space, rent less space or bring space back onto the market,” according to the report by Savills in Washington DC.

Total leasing activity declined 33% year over year to 1.2 msf. Almost half of these activities came from federal and local authorities.

Overall, the asking rent fell to 55.53 psf per year. “However, owners are aggressive about pricing, concessions and flexibility to attract and retain tenants,” the report said. “New Class A long term leases receive an average of $ 148.00 psf tenant improvement grants and 21 months of free rent. This corresponds to a total of 260.00 psf – an increase of a little more than 50.00 psf since the beginning of the pandemic – and significantly reduces the effective rent of the tenants. ”(Diagram via Savills).

As Houston has shown, the office markets can be in very difficult slumps for years as developers continue to build the newest and largest office towers. In Houston, despite years of burglary, there is still more than 3 msf of office space under construction, although this is 28% less than the 10-year average, according to JLL.

And when that sort of long slump occurs, there’s an escape to quality with businesses moving to the newest and tallest towers when their old lease expires and giving up older office buildings whose landlords eventually pull themselves off the mortgage and the lenders could let you worry about the collateral.

The question is not what to do with the latest and greatest office towers because they will always find tenants. The question is what to do with older office buildings whose tenants move out as part of the flight to quality, if the lease allows it. It is these older office towers – or rather their creditors – that will be in trouble if the break-in drags on.

Have fun reading WOLF STREET and would you like to support it? Using ad blockers – I totally understand why – but would you like to endorse the site? You can donate. I appreciate it very much. Click the beer and iced tea mug to find out how:

Would you like to be notified by email when WOLF STREET publishes a new article? Sign in here.

![]()